12 February 2021

There are many benefits to using a descriptor for a platform where many payments are made by bank card. Let’s take a look at this feature.

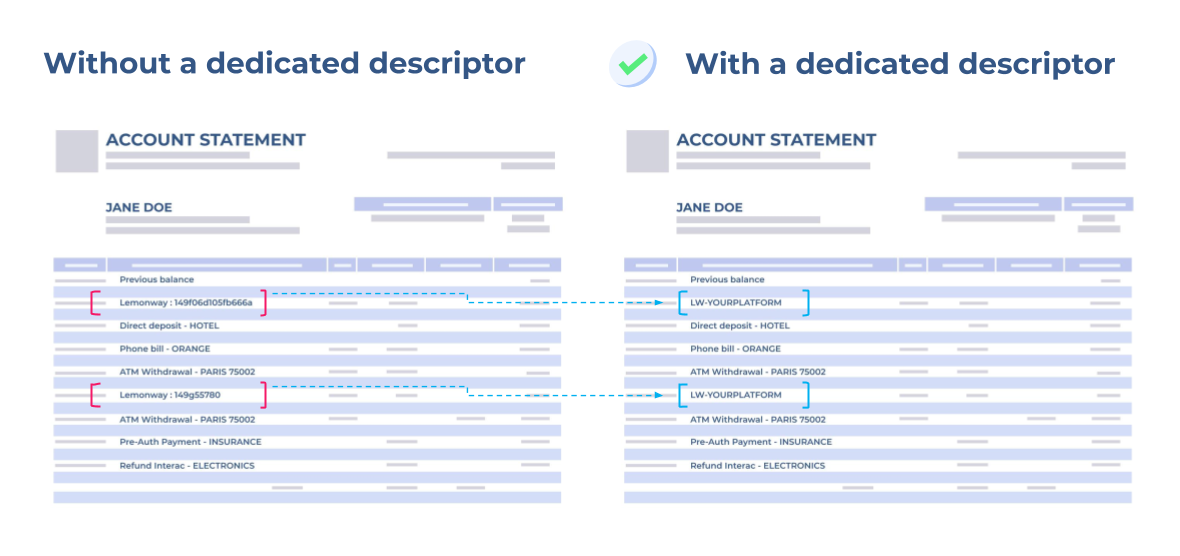

A descriptor is the wording that appears on the bank statement of the cardholder making the purchase. The concept of descriptor only applies to payments using a card. This is typically the name the buyer will see on their bank statement following a purchase from a B2C marketplace. With a default generic descriptor, it is generally the name of the PSP that appears, for example “LEMONWAY.COM/PI”.

In most cases, the end-customers of your platform know nothing about the payment service provider you are using. Without a dedicated descriptor, they will not know what such payment corresponds to. Some people will then perform a search on Google and come across an explanatory page, so they can trace the origin of the payment. Others will believe that the purchase is fraudulent and file a complaint with their bank. You then end up with a card chargeback and an unpaid debt, which could cost you dearly, especially if the complaints mount up.

So for a purchase amount of 10 euros, not only will the cardholder’s bank directly retrieve the purchase amount, it will also impose fixed incident costs.

Depending on your card payment volumes, the dedicated descriptor has many advantages. The B2C and C2C marketplaces are particularly affected, since a large number of buyers prefer to use a card to make their payments.

A dedicated or personalised descriptor firstly allows you to choose the 12-character wording of your choice, so that your customers instantly recognise the transaction when checking their bank account statement.

Thus, instead of the wording “LEMONWAY.COM/PI” appearing on their bank account statement, the customer will see “LW – YOUR PLATFORM”. This simple customisation greatly reduces the number of card chargebacks, while streamlining the customer journey.

Read also: 8 best practices to avoid chargebacks and unpaid debts

The advantages of using this option do not end there. In addition to reducing the number of unpaid debts, the use of a dedicated descriptor helps limit the risk of fraud. Without a dedicated descriptor, you end up sharing the same descriptor with the other clients of the PSP platform. This means it is not possible to fine tune your approach to risk.

The use of a dedicateddescriptor thus allows you to reduce your fraud rate by configuring a personalised fraud exposure according to your activity. Need more information on this product? Contact us!